Local Property Tax (LPT)

How does LPT affect employers?

Householders can opt to pay their Local Property Tax (LPT) in one single payment or to phase their payments over the period January to December. One of the phased payment options being made available is deduction at source from salary or occupational pension.

To opt for deduction from Irish Salary, Wages or Occupational Pension the property owner provides:

- Employer or Pension Provider’s Name.

- Employer or Pension Provider’s Tax Registration Number.

If this option is selected, payment will be spread evenly over the period 1st January to 31st December. The amount of each installment will depend on the number of salary, wages or pension payments the employee is due to receive in this period.

General Rules around making payment of the LPT through a salary deduction

- The Householder/employee cannot choose when the deduction starts. The employer must follow the instruction on the Tax Credit Certificate (P2C) issued by Revenue and is required to start the deduction from the next pay period after the date of receipt of the P2C.

- Once the LPT deductions commence, the employer is obliged to continue the deductions and spread them evenly over the remaining pay days in the year. The employee cannot request that the employer pause the deduction, nor can the employer make this decision either.

- Employers must collect the total LPT liability for the year by spreading it evenly over the remaining pay dates in the year.

- LPT cannot be deducted in any pay period for which the employee is not in receipt of payment. However, once salary payments resume employer will have to adjust the amount of LPT being deducted to ensure that the total liability is paid by the end of the tax year. This will result in a slight increase in the amount of LPT being deducted from the remaining salary payments in the tax year.

For Example

Original P2C states a total annual LPT deduction of €120 for the tax year (the P2C will not indicate a periodical deduction)

Schedule of deductions from 01st January to 31st December for monthly paid employee.

Employee receives payment from January to May, with an LPT deduction of €10 applied to each monthly salary payment

€120 / 12 monthly salary payments = monthly deduction of €10

Employee takes unpaid leave for the months of June, July and August (3 months) without any salary payment

(5 months x €10)

(no payment from which to deduct LPT)

01st September

(4 months x €17.50)

- Once an LPT deduction instruction is issued to the employer to commence LPT deductions from an employees payroll an employee can arrange an alternative payment method with Revenue if they wish.This can be done by accessing the online filing system using your Property ID, PIN and your PPSN, or by calling the LPT Helpline on 1890 200 255. To establish how much LPT an employee/householder still has to pay for the tax year, the amount of LPT already paid by them through their wages (as confirmed on the payslip) should be subtracted from their total LPT liability for the tax year (as per P2C).

Once the new payment method is confirmed, Revenue will send an instruction to the employer to stop deducting LPT for that employee by issuing a new Tax Credit Certificate (P2C).

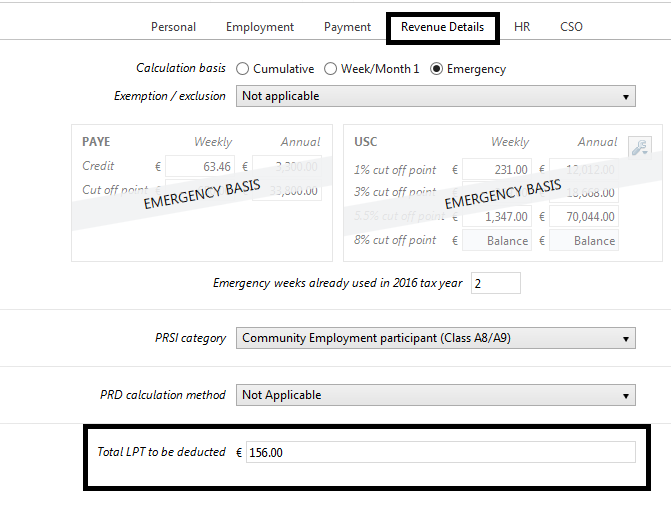

Applying the LPT deduction to an employee record

- Within BrightPay select the Employee record

- Choose Revenue Details

- Enter the ANNUAL LPT deduction in the dedicated field

- If you are importing your P2C from ROS, the LPT Revenue instruction will automatically import for each employee to which it applies from the P2C file. No further action is required by the employer.

Processing Pay

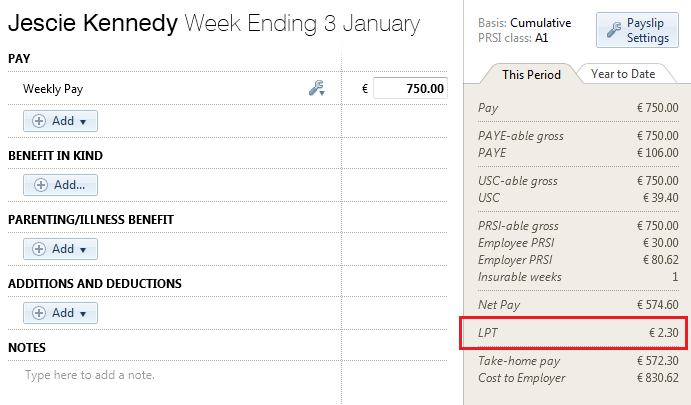

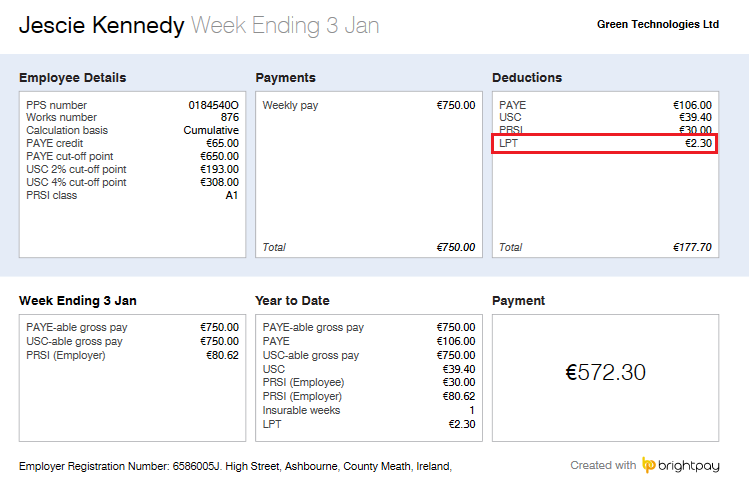

- Details of the LPT deduction must be recorded on the payslip to give a statement of deduction to the employee (as per the example below).

WHAT PRIORITY WILL BE APPLIED TO THE DEDUCTION OF LPT IN PAYROLL

- Where a Court Order is already made at the time of issuing the P2C (advising LPT deduction) the Court Order will take precedence over the LPT deduction. If the Court Order is made after the P2C (advising LPT deduction) has issued, the LPT deduction will take precedence.

- LPT takes precedence over all non-statutory deductions.

Need help? Support is available at 01 8352074 or [email protected].