EWSS - Overview

The Employment Wage Subsidy Scheme (EWSS) replaces the Temporary Wage Subsidy Scheme (TWSS) from September 1st 2020.

Comprehensive Revenue guidance has now been published with regard to the operation of the Employment Wage Subsidy Scheme which can be accessed here.

Please find below an overview with regard to how the scheme is to operate and to help you prepare for it should you choose to avail of it.

Employment Wage Subsidy Scheme - Overview

- The scheme provides a flat-rate subsidy to qualifying employers based on the number of paid and eligible employees on the employer’s payroll. The scheme is expected to operate until 31st March 2021

- Eligible employers will be required to register for the EWSS via ROS, registration has been available since August 18th.

- Employers must hold up to date tax clearance to register for the scheme and receive the subsidy payments.

- Employers must be able to demonstrate that their turnover or customer orders between 1st July and 31st December 2020 have suffered at least a 30% reduction as a result of Covid-19. Further information on the qualifying criteria can be found here

- Registered childcare providers can avail of the EWSS without the requirement to meet the 30% reduction in turnover or customer orders.

- Employers must review their eligibility status on the last day of every month to ensure they continue to meet the eligibility criteria, if they no longer qualify they should deregister for EWSS with effect from the following day (1st of the month).

- The Temporary Wage Subsidy Scheme (TWSS) will cease on August 31st 2020.

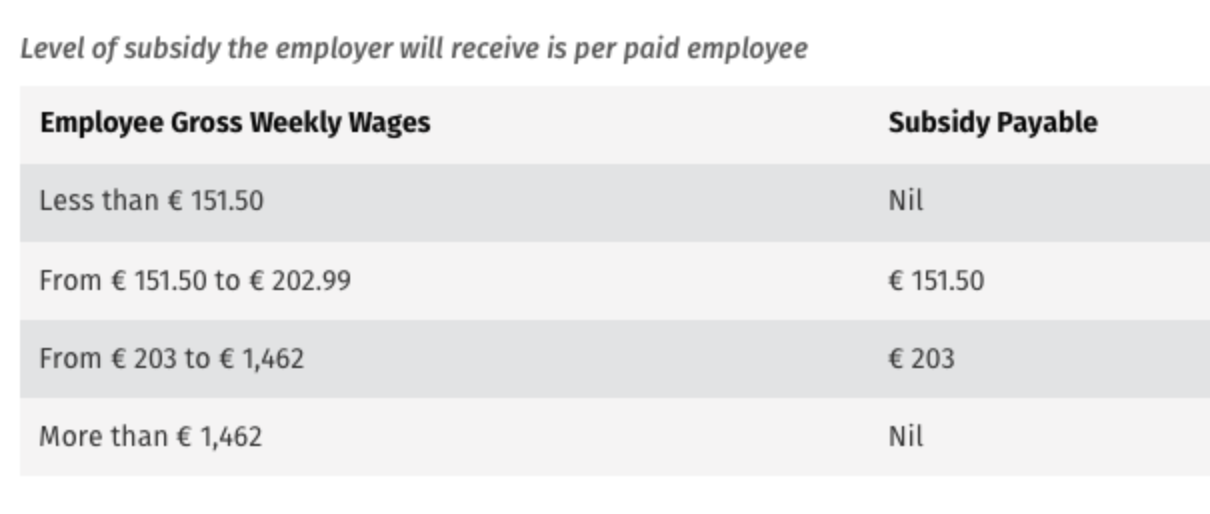

Subsidy Payment:

The rate of subsidy provided under the Employment Wage Subsidy Scheme (EWSS) has been revised to better support businesses dealing with Covid-19 Level 5 restrictions.

Broadly, the EWSS rates will be aligned with the rates of payment under the PUP. The following revised rates are effective from the next payroll date after October 19th 2020, they will revert to the previous rates from February 1st 2021.

Previous rates:

Please note: gross pay includes notional pay and is before any deductions for pension, salary sacrifice etc.

Frequency of EWSS payments:

The EWSS was originally designed to pay the subsidy due once a month in arrears as soon as possible after the due date of the relevant monthly Employer PAYE return (the 14th of the following month).

On 6 October 2020, Revenue announced that it had brought forward the date for EWSS payments to the fifth day of the following month. October EWSS payments, including the increased rates announced by the Minister for Finance in respect of payroll submissions with pay dates on or after 20 October 2020, will be paid by 5 November 2020.

Revenue is currently working to further significantly shorten the EWSS payment timeframe. In this regard, the first EWSS payments in respect of November payrolls will be made in early November, rather than by 5 December. Thereafter, subsequent payments for November will be paid following the receipt of a payroll submission containing an EWSS claim. This means EWSS will be paid on a similar basis to the Temporary Wage Subsidy Scheme (TWSS), providing a significant positive cashflow boost for businesses.

Due to the current Level 5 public health restrictions, employers who previously did not qualify for EWSS may now be able to show the necessary 30% reduction in turnover or customer orders between 1 July and 31 December 2020. Revenue is reminding employers that it is still possible to register for EWSS once all qualifying criteria are met. Once registered, employers can then claim subsidy payments in respect of payroll submissions with a pay date on or after their registration date.

Payroll:

- Under the EWSS, employers will be required to pay employees in the normal manner i.e. calculating and deducting Income Tax, USC and employee PRSI through the payroll.

- EWSS is a subsidy paid to an employer, it will not show on payslips or in myAccount.

Employer PRSI:

A 0.5% rate of employers PRSI will continue to apply for employments that are eligible for the subsidy, this is expected to work as follows:

- PRSI will be calculated as normal via payroll e.g. on PRSI class A1.

- Revenue will calculate a PRSI credit by calculating the difference between the rate on the normal class and the 0.5%.

- The credit will show on the Statement of Account to reduce the employer’s liability to Revenue.

Publication:

A list of employers availing of EWSS will be published in January 2021 and April 2021 to www.revenue.ie

Software Upgrade (to cater for EWSS):

An upgrade for BrightPay to cater for the Employment Wage Subsidy Scheme (EWSS) has now been released.

To view guidance on how to operate EWSS within BrightPay, please click here.

Need help? Support is available at 01 8352074 or [email protected].